Transparent and Purposeful - That's What We Do!

|

The treasurer is one of the three elected officers required to have a PTA/PTSA.

This lucky elected officer is responsible for documenting and managing the fiscal operations of the unit, council, and district PTA, and is the authorized custodian of all funds for the respective PTA. The treasurer is also responsible for keeping appropriate records of the financial activity of the unit, and preparing and presenting reports and filings in compliance with local state and federal laws. Don't Forget! The treasurer's authority as an elected officer only lasts for the length of their term! Once the term is over, the outgoing treasurer cannot pay bills or act on behalf of the unit. Once the year changes, it's time for treasurer-elect to ensure authorized bills are paid, deposits made, and that everything is documented appropriately. |

BudgetBefore funds can be spent, the PTA/PTSA must create a budget, and have that budget adopted by the general association (membership) of the PTA. The funds to be spent must also be "released" by the general association. Releasing funds from one meeting of the general association to the next is the general association giving permission for funds to be spent!

Let’s Walk Through It: Both the Executive Board and the General Association vote in financial matters. Each voting body has a role to play!

The budget is flexible. Need to change it? Amend it! Add or remove programs or fundraisers or shift funds from one line item to another. Just make sure that it is approved by the executive board and the general association. There must be a 2/3 vote of approval for budget amendments to be adopted.

The Executive Board is the “Planning Team.” The General Association is the “Boss,” and recording it in the minutes is what makes the legal record!

Can We Write this Check? [click the link for the handout]

When planning programs and events, ask these questions:

Financial Reporting |

|

Annual Reports

Coming soon...

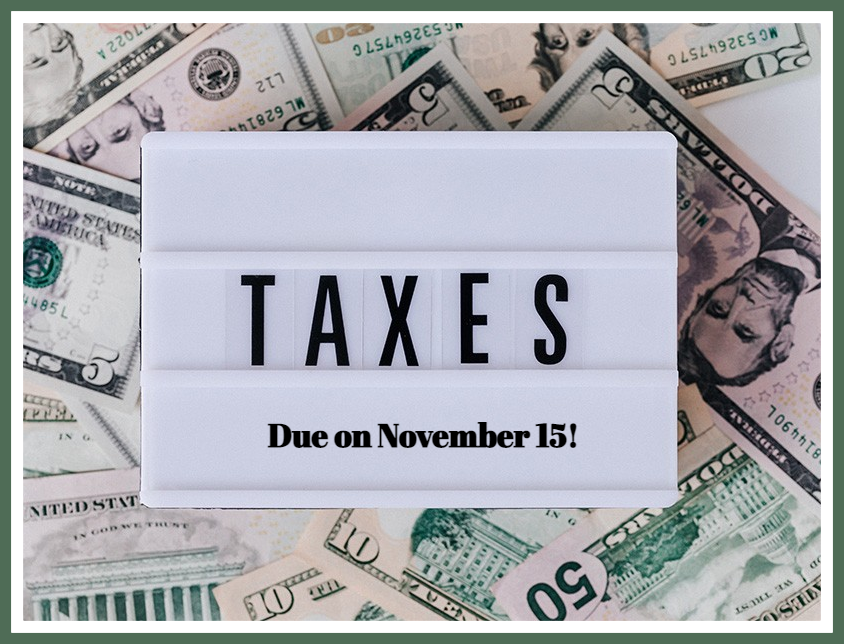

Filing TaxesAll units are required to file taxes annually (regardless of annual revenue.) - this is a vital piece of keeping our businesses legally operating and compliant.

Taxes must be filed by the 15th day of the 5th month after the close of the fiscal year. The fiscal year for all 23rd District PTA's ends on June 30, which means taxes must be filed by November 15th annually. What To File: If your unit/council has an annual revenue exceeding $50,000 annually:

If your unit/council has an annual revenue under $50,000 annually:

|

|

Attorney General (State of California)Every unit must file the Annual Registration Renewal Report (RRF-1) every year. This can be done at the same time as tax filing preparation, and if the unit's gross receipts exceed $25,000 for the year, there will be an associated fee. This filing uses the RCF (Registry of Charities and Fundraisers [formerly Registry of Charitable Trusts] Number) found in the unit bylaws.

Don't Forget!

Look It Up! Registry of Charities and Fundraisers (Formerly Registry of Charitable Trusts) RRF-1/RRF-1 (Annotated) CT-TR-1/CT-TR-1 (Annotated) Raffles Is your unit or council interested in holding a raffle? Make sure you have a permit! CT-NRP-1 (Raffle Permit)

CT-NRP-2 (Raffle Report)

Q. What's the difference between an opportunity drawing and a raffle? A. An opportunity drawing is a drawing or giveaway where everyone has an equal opportunity to win, just by being there! No one has to purchase a ticket or an item at the event to qualify to win. A raffle involves the exchange of money for an increased chance of winning. For example, if an attendee gets an opportunity to win just by attending, and gets another opportunity to win by purchasing a funnel cake (or another ticket), that is a raffle, and the unit must have a permit. If you aren't sure, be safe and reach out and ask for clarification! Q. Can we conduct a raffle online? What can we do online? A. Unfortunately, no. You may release information on your raffle online (the date the raffle will occur, how much tickets will be and where they will be sold, as well as the terms and conditions for participating; however, the conducting of the raffle itself, nor the purchase of tickets (or opportunities to get increased chances) may be done online. Don't forget! Raffle tickets must be two-part detachable tickets only. Q. Where can I find more information on holding a compliant raffle? Holding a compliant raffle is not something that is governed by PTA. The primary information can be found by at the California State Attorney General's Office website, California State Penal Codes 320.5 and 320.6, and the California State PTA Toolkit, all of which are fantastic resources to help ensure your raffle (or opportunity drawing!) is not only amazing, but legal! Worker Compensation Annual Payroll ReportThe Worker Compensation Annual Payroll Report form must be filed annually, regardless of whether or not the individual PTA paid employees. The California State PTA insurance company, AIM Insurance Services, has made this process easier than ever - submission can be completed online!

This report must be filed by January 31 annually, and covers the previous calendar year (not fiscal) Click the link to file the Worker Compensation Annual Payroll Report. Click here to find more information on insurance and requirements at CAPTA.org, as well as the current Insurance Guide. |

|

Need something that you aren't seeing?

Check out the California State PTA Tax Filing Support Center

Still need help? Reach out!

You can find the 23rd District Treasurer at [email protected]

Check out the California State PTA Tax Filing Support Center

Still need help? Reach out!

You can find the 23rd District Treasurer at [email protected]